Revenue growth tells you that customers are coming in. Unit economics tells you whether those customers are worth more than it costs to get them. A business can be growing fast and destroying value at the same time, and without the CAC-to-LTV ratio, the two look identical from the outside.

The ratio is simple: divide lifetime value by customer acquisition cost. If the result is 3 or higher, the business is covering what it costs to acquire customers and generating enough margin to sustain itself. Below 3, something is broken, and scaling will make it worse, not better. Below 1, the business is paying more to acquire customers than those customers will ever return.

What the ratio cannot tell you on its own is how long it takes to recover the acquisition investment. That is the payback period: the number of months before a customer's gross margin contribution covers what it costs to acquire them. A healthy ratio with a long payback period creates cash flow pressure that can stall growth just as effectively as poor unit economics. Both measures together give you the complete picture of whether your business model can support the growth you are planning.

What unit economics measures

Unit economics is the discipline of understanding the economics of a single unit. In most businesses, that unit is a customer. The question it answers is: after accounting for all the costs to acquire and serve a customer, do we actually make money on them?

This matters because revenue growth and healthy unit economics are not the same thing. A company can grow revenue at 100% year on year while losing money on every customer it acquires. Revenue growth means customers are coming in. Unit economics tells you whether acquiring those customers is creating or destroying value. Conflating the two is one of the most expensive mistakes a founder can make, because it means scaling a broken model and amplifying the losses with every new customer.

The unit in unit economics is not a product, a transaction, or a department. It is a customer relationship from acquisition to the end of life. A sales lead at a SaaS company who celebrates closing 50 new deals in a quarter without knowing the CAC or LTV of those deals is celebrating a number with no context. Unit economics gives that number its meaning and tells you whether the growth is real or just expensive.[1]

The 3:1 ratio threshold

The CAC-to-LTV ratio is calculated by dividing lifetime value by customer acquisition cost. A company with a CAC of 1,500 euros and an LTV of 6,000 euros has a ratio of 4:1. For every euro spent acquiring a customer, that customer generates 4 euros in lifetime value.

The minimum threshold for a healthy business is a ratio of 3:1. This is not an aspirational target. It is the floor below which there is not enough margin left to cover the organizational overhead that sits outside of CAC and LTV: the product team, the leadership, the infrastructure, and the inevitable experiments that any growing company requires. At 1:1, every euro spent acquiring a customer is returned in full, with nothing left over for anything else. At ratios below 1:1, the business is paying more to acquire customers than those customers will ever generate, regardless of how fast revenue is growing.

A ratio well above 3:1 is not always a signal to celebrate, either. If the ratio is 10:1 or higher, the company may be underinvesting in acquisitions, leaving growth on the table that the unit economics could support. The ratio is a guide for investment decisions in both directions, not a trophy.[2]

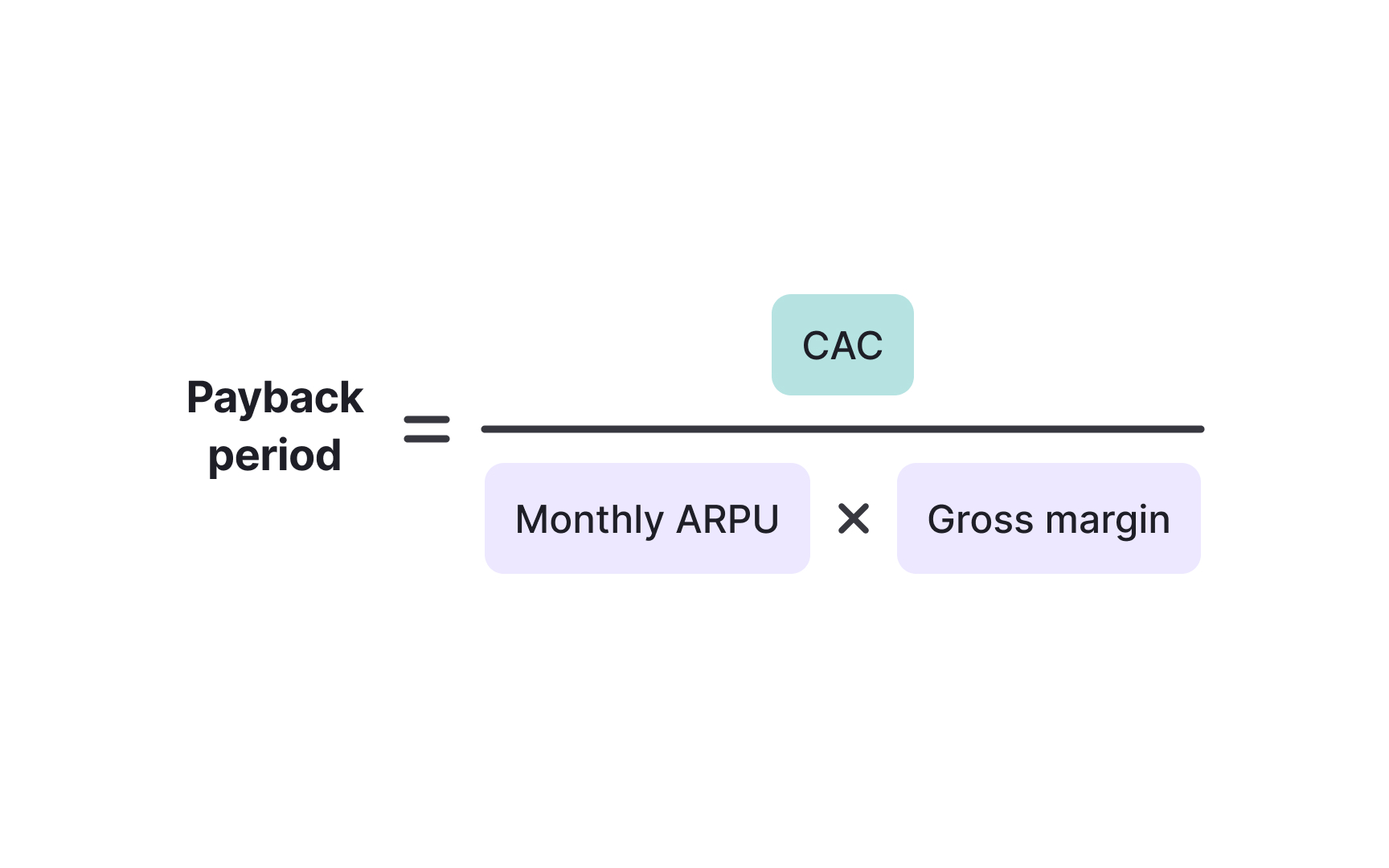

The payback period

The payback period is the number of months it takes for a customer's gross margin contribution to recover the cost of acquiring them. The formula is: CAC divided by monthly average revenue per user (ARPU) multiplied by gross margin. A company with a CAC of 2,400 euros, 200 euros monthly ARPU, and 75% gross margin has a payback period of 2,400 divided by 150, which equals 16 months.

Payback period matters independently of the LTV-to-CAC ratio because it measures timing, not ultimate return. A business with an excellent ratio but a 24-month payback period is fronting the acquisition cost today and recovering it over 2 years. During that window, every new customer acquired creates a cash outflow before it creates an inflow. The faster a company grows, the larger that gap becomes.

For most businesses, a payback period under 12 months is acceptable. Under 6 months is strong. Above 18 months creates real cash flow pressure, because the company is effectively financing the gap between spending and recovery. For early-stage companies without deep reserves, a long payback period is one of the most common reasons that growth stalls: the business runs out of cash to fund new acquisitions before existing customers have paid back their cost.

Unit economics by channel and segment

Not all customers produce the same unit economics, and not all channels produce customers with the same economics. Calculating a single ratio across all customers and channels hides the information that actually drives decisions.

A company with 2 acquisition channels might find that enterprise customers acquired through direct sales have a CAC of 10,000 euros and an LTV of 70,000 euros, producing a ratio of 7:1. Small and medium-sized business (SMB) customers acquired through paid search might have a CAC of 400 euros and an LTV of 800 euros, producing a ratio of 2:1. The combined ratio sits somewhere in the middle and looks acceptable. The channel-level picture shows that one channel is building the business and the other is consuming resources below the minimum threshold. Without this breakdown, a growth lead might recommend increasing paid search spend because the overall economics look healthy. With it, the decision is clear: invest more in the channel producing 7:1 returns and either fix or reduce investment in the channel producing 2:1. Channel-level and segment-level unit economics is not a nice-to-have analysis. It is how resource allocation decisions get made rationally.[3]

Pro Tip! Calculate channel-level unit economics before increasing spend, not after. Scaling reveals problems that blended numbers were hiding.

3 levers for fixing unit economics

When unit economics are below the 3:1 threshold, there are 3 levers available. Each targets a different part of the calculation:

- Reducing customer acquisition cost (CAC) means finding more efficient ways to acquire customers. This might mean shifting budget toward channels with lower acquisition costs, improving conversion rates so existing spend produces more customers, or tightening targeting so fewer unqualified leads consume sales resources.

- Increasing LTV means getting more value from customers who have already been acquired. The two most direct paths are reducing churn, so customers contribute over a longer period, and increasing average revenue per user through pricing adjustments or upsell. Both raise the numerator in the ratio without touching the acquisition cost.

- Changing the business model is the hardest lever and becomes necessary when neither CAC nor LTV can be moved within the current structure. This might mean serving a different customer segment with better unit economics, changing the pricing model, or restructuring the product to reduce the cost of delivery.

What it should never mean is ignoring the problem and scaling through it. More volume at a broken ratio does not fix the economics. It amplifies them.[4]

When unit economics support scaling

Unit economics are the test that determines whether scaling is appropriate. Scaling means investing significantly more in customer acquisition: more sales headcount, more marketing spend, more channel investment. It only makes sense when unit economics confirm that more acquisition creates more value rather than more losses.

The test has two parts:

- Are CAC and LTV stable at the current scale? If both are holding, scaling is likely to produce similar economics at higher volume.

- What happens to those numbers as acquisition spend increases? CAC tends to rise with scale because companies exhaust their most efficient channels and move into progressively less efficient ones. If CAC is already rising as spend increases modestly, projecting that trend forward shows what the economics will look like at double or triple the current spend.

A company that passes both parts of this test has evidence that its growth investment will compound. A company that fails either part is not ready to scale, regardless of how strong the top-line growth looks. A growth lead who commits to significant investment without running this analysis is moving fast without knowing whether the economics support the speed.[5]

Pro Tip! CAC almost always rises as you scale. Build that assumption into your projections rather than hoping current efficiency holds.

Revenue growth vs. viable unit economics

A business with strong revenue growth and failing unit economics has not yet discovered it has a problem. The ratio and the payback period together answer the only question that ultimately matters: is this business model viable?

Viability does not mean profitable today. Early-stage companies routinely invest ahead of profitability, and that is rational when the unit economics support it. A company with a 4:1 LTV-to-CAC ratio and a 10-month payback period is making a bet that is backed by actual numbers. The investment in the acquisition will return 4 times its cost within a reasonable timeframe. That is a projection grounded in real customer behavior, not optimism.

A company with a 1.5:1 ratio and an 18-month payback is making a different bet: that future improvements in CAC or LTV will rescue the economics before the cash runs out. That bet can be right, but it requires acknowledging that the current model does not work and having a specific plan to fix it. The founders who get into trouble are not the ones who have bad unit economics. They are the ones who do not know they do, or who know and scale anyway, hoping that volume will solve what the numbers are already telling them it will not.[6]

Unit economics as the GTM feedback loop

Unit economics does not make every decision for a business, but it disciplines the decisions that involve allocating scarce resources. When you know which channels and segments are creating value and which are destroying it, you can stop being polite about where you invest.

This is the final checkpoint in the go-to-market system. A company with excellent positioning, a well-designed channel strategy, value-based pricing, and good market timing will still fail if the economics of each customer relationship do not work. A company that knows its unit economics, in detail, by channel and segment, has the information to make rational decisions about where to grow and how fast.

The GTM system is only coherent when unit economics validates or challenges each piece of it. Positioning that attracts customers with low LTV needs to be revisited. A channel producing a 2:1 ratio needs to be fixed or cut. A pricing model that produces good LTV but excessive payback needs to be restructured. Unit economics is not the end of the analysis. It is the feedback loop that tells you whether everything else is working.[7]

Topics

References

- A Practical Guide to CAC and LTV for B2B SaaS Marketers | Gripped

- CAC SaaS: A guide for businesses | Stripe

- LTV/CAC Ratio | SaaS Formula + Calculator | Wall Street Prep

- CAC vs. LTV: Misalignment Risks - Phoenix Strategy Group

- A Practical Guide to CAC and LTV for B2B SaaS Marketers | Gripped

- Unit Economics 101: Using CAC and LTV to Guide Pricing Strategy

- CAC/LTV Guide: Calculate & Optimize Customer Unit Economics | PM Toolkit | PM Toolkit